AMZ123 Cross-border e-commerce

AMZ123 Cross-border e-commerceAuthor | Shuangmu@AMZ123

Statement | This article is copyrighted by AMZ123 and may not be reproduced without permission.

The year 2026 is destined to be a challenging one for cross-border sellers.

The supply chain dilemma affected by the situation in the Middle East has not been alleviated, and recently, the United States has swung the "trade war" hammer again, making the already uncertain global trade environment even more complex and turbulent, adding another "tight spell" to the heavily pressured cross-border sellers.

AMZ123 has learned that on March 11, local time, the Office of the United States Trade Representative (USTR) announced that the U.S. Trade Representative has officially initiated a Section 301 investigation against 16 trading partners, including China, the European Union, Mexico, Vietnam, India, and Japan.

The so-called "Section 301 investigation" originates from Section 301 of the U.S. Trade Act of 1974. This provision authorizes the U.S. Trade Representative to initiate investigations into "unfair and unreasonable trade practices" by other countries and, after the investigation concludes, may propose recommendations for implementing unilateral sanctions.

USTR claims that the initiation of the Section 301 investigation is aimed at trade practices such as "excess manufacturing capacity and unfair industrial subsidies," but the industry generally believes that the direct trigger for the investigation is the U.S. Supreme Court's ruling last month that the "reciprocal tariffs" imposed by Trump based on the International Emergency Economic Powers Act (IEEPA) were illegal, and it is speculated that if the investigation is implemented, tariff increases are inevitable.

According to the statutory process announced by USTR, this round of Section 301 investigations has entered the public comment collection stage, and a public hearing will be held from May 5. The U.S. side may form a final investigation conclusion in late July.

Looking at the implementation rules of previous U.S. Section 301 investigations, once it is determined that the investigated party has "unfair trade practices," the United States may impose restrictive measures such as high tariffs, import quantity restrictions, and strengthened qualification reviews. Therefore, after the announcement, many cross-border sellers who have深耕美国市场的跨境卖家都对“关税有可能再度上涨”一事感到忧心忡忡。cross-border sellers with a deep presence in the U.S. market are worried about the possibility of rising tariffs.

“手中无牌,又在虚空造牌。”

“关税不会又要涨了吧,能不能换个招啊。”

The announcement shows that the areas covered by this investigation include aluminum products, automobiles, batteries, cement, chemicals, electronic products, energy products, glass, machine tools, machinery, plastics, processed foods and beverages, robots, solar components, steel, and transportation equipment, many of which are core categories of Chinese cross-border e-commerce exports to the United States.

In addition, logistics experts point out that after the initiation of the Section 301 investigation, U.S. customs may also strengthen the verification of the country of origin, value, category, and production qualifications of goods. However, the cross-border e-commerce industry has long had behaviors such as vague declaration, underreporting of goods value, and irregular marking of the country of origin, which are likely to become the focus of customs crackdowns, with the probability of goods detention, return, and fines rising geometrically.

However, AMZ123 understands that, according to the website of the Ministry of Commerce, the sixth round of Sino-US economic and trade consultations will be held from March 14 to 17, and He Lifeng, member of the Political Bureau of the CPC Central Committee and Vice Premier of the State Council, will lead a delegation to France to hold economic and trade consultations with the United States.

Before the consultations are over, there is still a chance for a turnaround.

Compared to the pending results of the Section 301 investigation, more cross-border sellers are currently concerned about news related to U.S. customs supervision.

A wave of unrest, another wave arises.

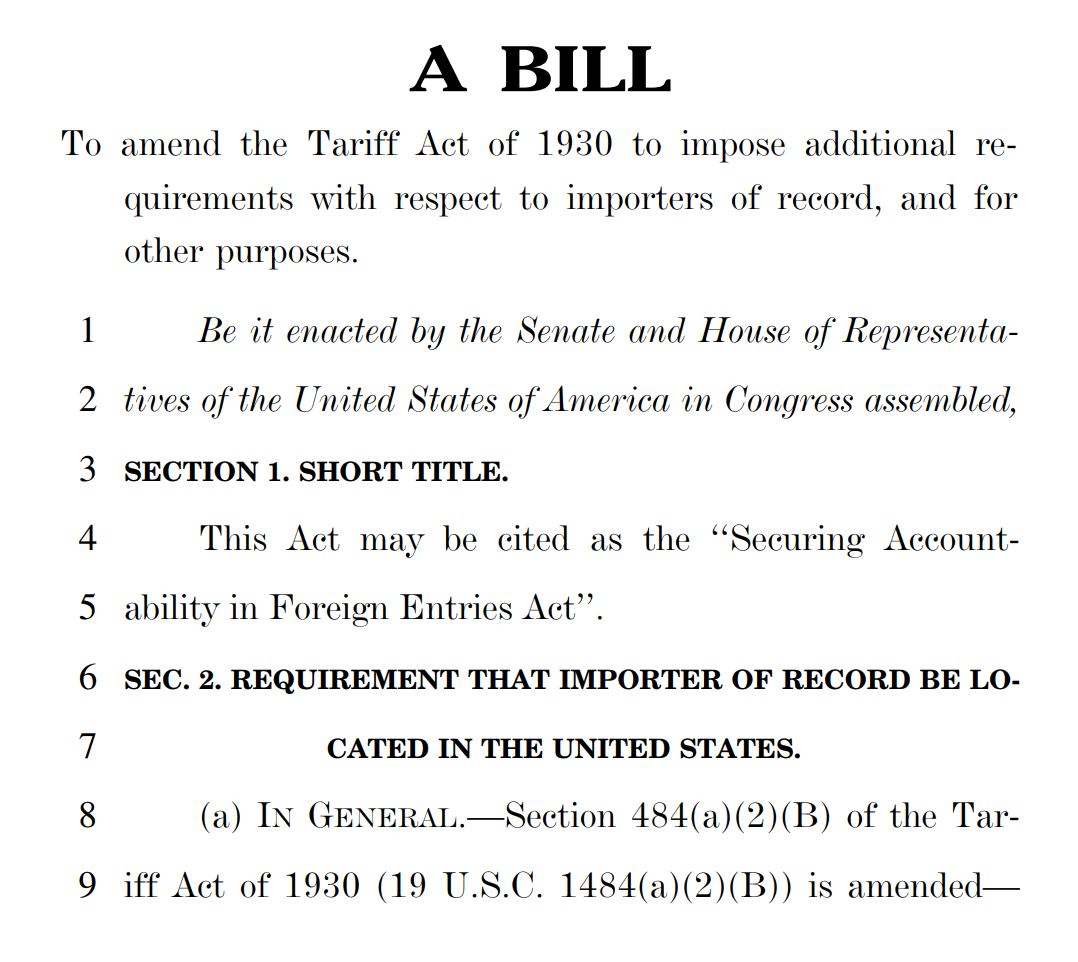

Just as the 5H inspection upgrade controversy was not yet settled, on March 9, local time, a U.S. senator from the Senate Judiciary Committee proposed a bicameral bill called the "Safe Imports Accountability Act" (abbreviated as the "SAFE Act"), which sparked heated discussion in the industry.

Public documents show that the bill imposes several requirements on importers' qualifications, tariff payment processes, and import bonds.

1. Qualifications

Individual qualifications: Must be a U.S. citizen or a legally permanent resident alien, and one individual can only act as a registered importer for one entity.

Corporate entities must meet one of the following conditions:

① A company with a physical operating address in the United States, with at least one full-time U.S. citizen or green card holder employee;

②A subsidiary of a U.S. company, which must have been operating for more than 3 years, with at least 1,500 employees and an annual revenue of $1 million, and must be registered with customs and bear joint legal responsibility.

③A company established under the laws of Canada, Australia, or a "qualified country."

2. Tariff Payment Process

Tariffs must be paid from a bank account that has completed the anti-money laundering customer identification verification process, and this process must be completed before the first customs declaration by the new importing customs broker. At the same time, importers need to provide their bank account and routing number to U.S. Customs and Border Protection (CBP).

3. Import Bond

For registered importers using a continuous import bond, a bond of no less than $100,000 must be maintained, which must be established in the importer's own name and used only for their own import business. New bonds issued within 60 days after the bill takes effect must meet the standards, and existing bonds must be renewed within 360 days, with non-compliant existing bonds being required by customs to be supplemented.

From industry discussions, once the bill is officially implemented, it will have a significant impact on cross-border sellers in the U.S. market.

On the one hand, if cross-border sellers cannot meet the bill's strict requirements for registered importers' U.S. entity presence, local personnel, and compliant accounts, they will no longer be able to act as importers, significantly reducing their control over the customs clearance process, or incurring additional compliance commission fees.

On the other hand, some gray customs clearance methods previously used by some cross-border sellers, such as "dual clearance and tax-inclusive" and "shared Bond/tax number," may suffer severe blows, and violators will have to bear high costs for return shipment and port detention.

As of the time of publication, the bill is still in the legislative stage, with uncertainties due to the gaming of stakeholders.