Cross-border e-commerce Hugo.com

Cross-border e-commerce Hugo.com

Recently, the U.S. trade policy has released two major signals: on the one hand, the U.S. Customs announced that it will start the tax refund arrangement in April; on the other hand, the U.S. government restarted the "Section 301 investigation", including 16 countries and regions such as China, the European Union, and Japan in the investigation scope. The two policies appeared almost at the same time, making the cross-border e-commerce industry once again feel the complexity and variability of the policy environment, which also means new uncertainties are brewing for cross-border sellers relying on the U.S. market.

For tens of thousands of U.S. importers (sellers) who have been waiting for a year, April this year will be a historically significant turning point.

Due to the previous unconstitutional ruling by the U.S. Supreme Court on the tariffs imposed under the International Emergency Economic Powers Act (IEEPA), the U.S. Customs and Border Protection (CBP) has finally finalized the tax refund schedule under legal pressure. From mid-to-late April, the Customs ACE system will officially launch the automated recalculation module.

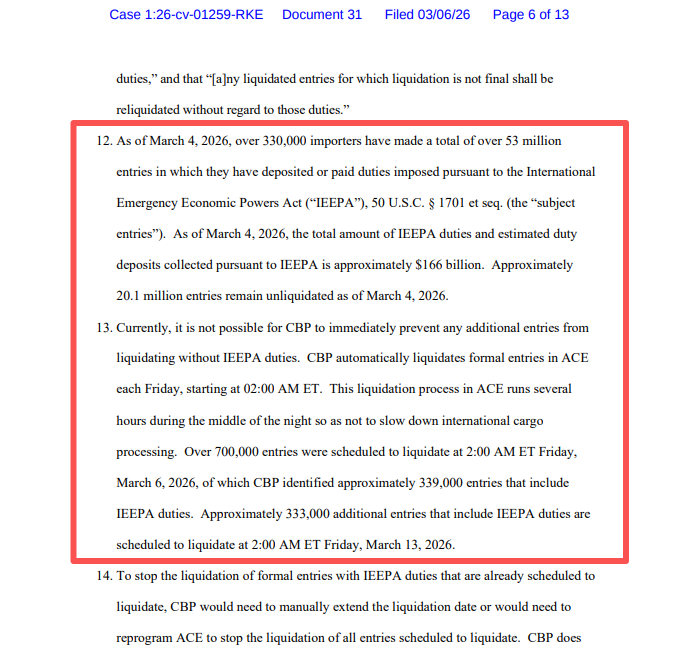

Screenshot: CBP Court Documents

According to documents submitted by the U.S. Customs to the court, as of early March 2026, more than 330,000 importers have paid tariffs under the relevant policy, with a total of more than 53 million import declaration records, amounting to approximately $166 billion. These tariffs are mainly targeted at goods imported from China and other places, affecting many cross-border e-commerce platform sellers, such as small and medium-sized exporters on Amazon, eBay, and Shopify.

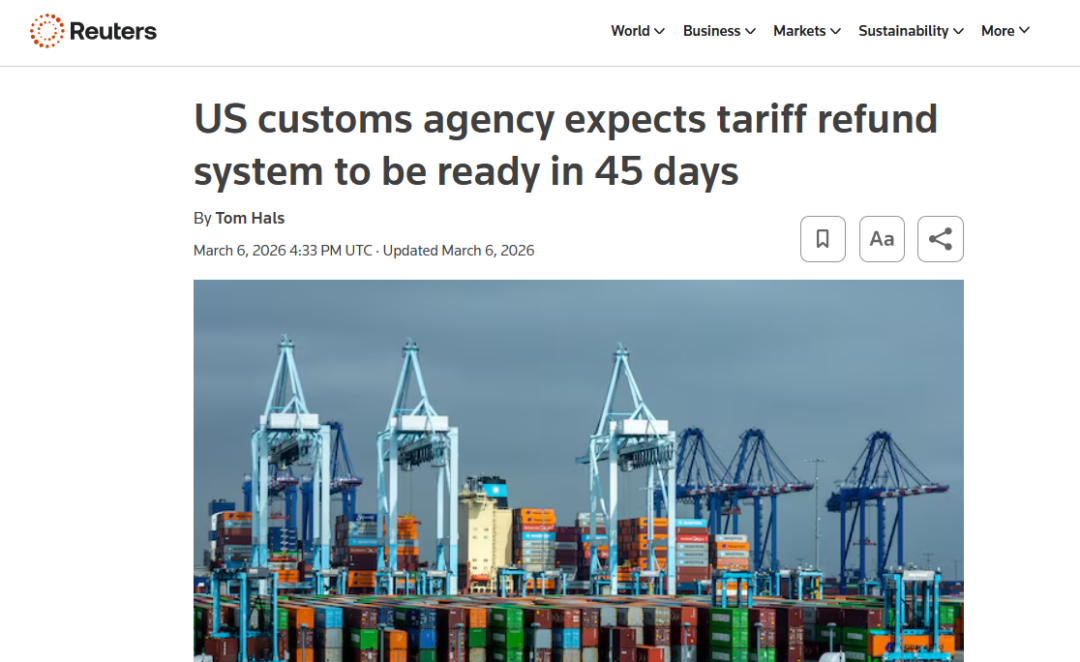

Screenshot: Reuters

CBP stated that due to the huge volume of tax refunds, a new tax refund module needs to be added to the ACE system, which is expected to go online within 45 days. The new process will allow companies to submit refund applications or confirmation information through an online portal, and the system will automatically calculate the refund amount and issue it in one lump sum.

It is reported that the U.S. federal trade judge has approved the postponement of immediate refunds to avoid system crashes. This means that after the launch in April, refunds will be issued in batches, with priority given to registered users. However, according to Reuters, as of early March, among the 330,000 importers eligible for refunds, only about 21,000 have completed electronic refund registration, which means that a large number of sellers still need to complete account settings to receive refunds smoothly.

For cross-border sellers, the top priority is to verify the import declaration information for the past two years as soon as possible to ensure the completeness of the information, including whether the HS code is consistent, whether the IOR is correctly attributed, whether the customs broker information is complete, whether the entries are in an unliquidated state, whether there are final entries, etc., all of which will directly affect the speed of refund. For sellers using customs clearance agents, it is especially necessary to confirm with the freight forwarder whether they are on the tax refund list and how the refund will be attributed.

The industry generally expects that CBP may announce more detailed refund procedures in April, including refund order, payment method, abnormal entry handling mechanism, whether appeals are allowed, and other implementation rules. It is recommended that sellers pay close attention to the progress of policy implementation to ensure timely participation in the refund process.

While the tax refund policy is gradually being implemented, another trade policy announcement by the U.S. government has cast a shadow over the global cross-border trade market. The restarted Section 301 investigation not only has a wide coverage but is also highly targeted, creating a policy contrast with the tax refund policy, further intensifying the uncertainty in the development of the cross-border e-commerce industry.

On March 11, local time, the Office of the U.S. Trade Representative officially announced that, in accordance with Article 301 of the 1974 Trade Act, a new round of "Section 301 investigations" will be initiated against 16 major trading partners, including China, the European Union, Japan, South Korea, India, and Mexico.

It is reported that the initiation of this Section 301 investigation is also due to the previous ruling by the U.S. Supreme Court that its "reciprocal tariffs" policy is unconstitutional. The U.S. has turned to Article 301 as an alternative tool, imposing a temporary tariff of 10% for 150 days according to Article 122 of the law as a transitional measure during the investigation period.

The U.S. claims that the investigated countries have flooded the global market with low-priced goods through government subsidies, harming the interests of U.S. producers. After the investigation is completed, new tariff measures may be introduced. It is expected that new tariffs will be imposed on some economies before this summer. The entire investigation process is characterized by "tight schedule, wide scope, and strong targeting."

At present, the most direct impact of this investigation is the significant increase in policy uncertainty and the continuous rise in compliance risks for cross-border sellers.

Essentially, the Section 301 investigation is a unilateral trade protection tool of the U.S. The policy adjustments during the investigation process are highly random, and the U.S.'s definition of "unreasonable trade practices" is subjective. It may expand the investigation scope and adjust the review standards at any time, leading to stricter inspections of goods during customs clearance, such as higher requirements for compliance documents like certificates of origin and production process records. If sellers fail to adapt to policy changes in time, they may face risks such as goods being detained, fines, or even being prohibited from entering the country.

Therefore, in the face of rising policy uncertainty, cross-border sellers need to take precautions against risks in advance. First, they can seize the opportunity to improve cash flow brought by the tax refund policy to accelerate capital recovery and ease operational capital pressure. Secondly, continuously optimize the product structure, reduce the proportion of high-risk categories, and enhance anti-risk capabilities.

More importantly, it is recommended that sellers conduct a comprehensive assessment of the potential impact of the Section 301 investigation and develop targeted response plans. At the market level, it is